ОБЗОР НА AAVE: ИНСТРУКЦИЯ ПО РАБОТЕ С БИРЖЕЙ

Внимание! Данная статья носит исключительно информационный характер и не содержит инвестиционных рекомендаций и советов по торговле.

Обзор подготовлен командой бесплатного терминала для торговли криптовалютой CScalp. Чтобы получить CScalp, оставьте свой электронный адрес в форме ниже.

Что нужно знать об Aave

Проект Aave создан в 2017 году на базе блокчейна Ethereum. Изначально протоколы Aave предназначались для лендинга и кредитования только c ETH. С появлением рынка децентрализованных финансов (DeFi), сервис провел ребрендинг и расширил возможности: теперь пользователям доступно более 20 токенов.

Кредитование и депонирование работает через пулы ликвидности. Вкладчики замораживают токены в пуле, зарабатывая на процентах и комиссиях. Заемщики берут кредиты, получая дополнительные активы. Для кредитования необходимо открыть депозит – он станет залогом в сделке.

На пулах ликвидности основан другой финансовый инструмент Aave – DEX-биржа. Торговля проходит через автоматический маркет-мейкер (АММ). Для торгов нужно иметь хотя бы один депозит. Эта особенность позволяет увеличить ликвидность и снизить проскальзывание сервиса Aave Swap.

Функционирование биржи обеспечено токеном AAVE формата ERC20. Поставщики ликвидности получают вознаграждение в AAVE. Эти токены используются в голосованиях по изменению основных протоколов сервиса. Ранее AAVE имел тикер LEND, но после ребрендинга сообщество решило снизить общую эмиссию. Теперь Aave совершает «миграцию» по фиксированной ставке 100 LEND = 1 AAVE.

AAVE — Обзор DeFi платформы

Aave отличается от других кредитных платформ тем, что представляет собой протокол с открытым исходным кодом и не хранит средства пользователей, обеспечивая децентрализованное финансирование (DeFi) на основе прозрачной инфраструктуры. В команде проекта 18 специалистов, штаб-квартира расположена в Лондоне. Название платформы — финское слово «призрак», символизирующее прозрачность.

Возможности платформы

Aave позволяет пользователям брать кредиты под залог криптовалюты и отдавать свою криптовалюту под проценты. При этом используется сочетание фиксированных и переменных процентных ставок.

- Сервис работает только с криптовалютами и стейблкоинами, фиат получить нельзя.

- Протокол реализован в виде набора смарт-контрактов на блокчейне Эфириум. Смарт-контракты обеспечивают безопасность и отсутствие необходимости в посреднике. Пользователи удобным им способом взаимодействуют напрямую со смарт-контрактами.

- В дополнение к обычным кредитным функциям, Aave предлагает ряд дополнительных, таких как кредиты без обеспечения и «переключение ставок».

- Протокол Aave разрабатывается с учетом всех надлежащих мер безопасности и проверяется несколькими аудиторами.

- Средства пользователей не контролируются третьей стороной, процесс полностью децентрализован.

- Токен LEND позволяет получить скидку на проценты по кредиты или повысить проценты по депозиту, а также ряд других преимуществ.

- Чтобы пользоваться Aave, необходимо иметь внешний кошелек (программный или аппаратный), такой как Coinbase или Ledger, поскольку деньги не хранятся в системе, а переходят непосредственно с кошелька на кошелек между пользователями.

Изначально платформа была запущена в 2017 году под именем ETHLend; в ноябре провели ICO, которое привлекло $600 000. В сентябре 2018 был произведен ребрендинг в связи с добавлением новых функций, в частности, работы с Биткоином.

Кредитование

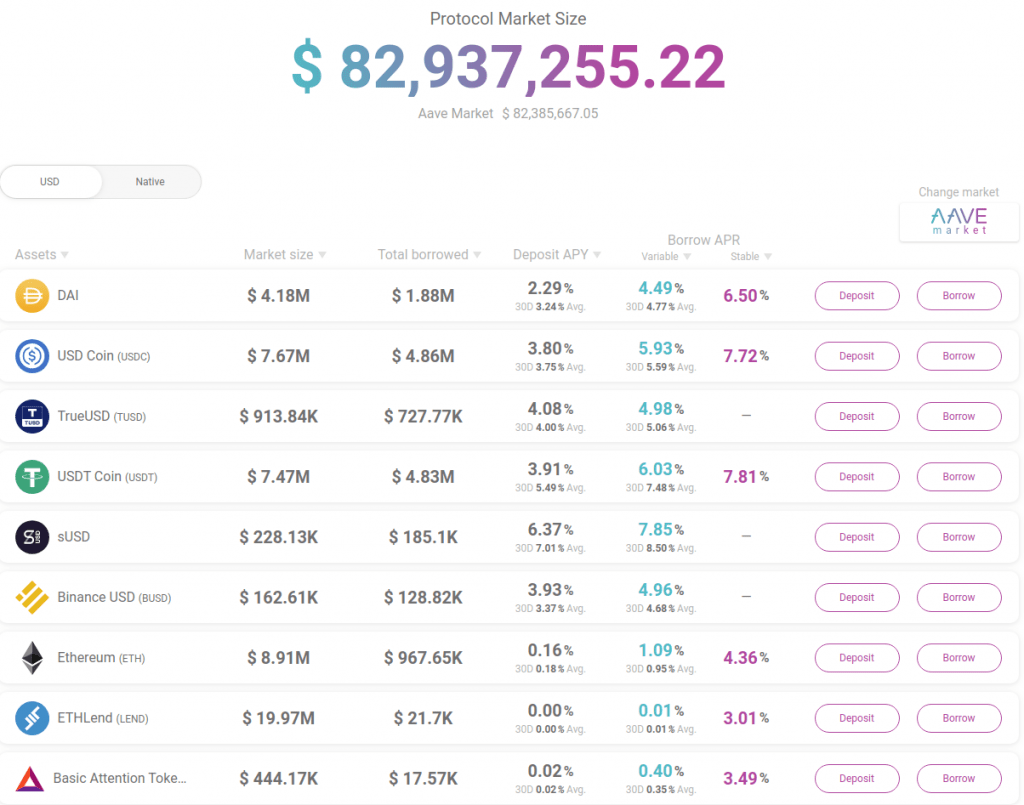

Чтобы взять кредит на Aave, нужно зайти в раздел Borrow и нажать соответствующую кнопку рядом с тем активом, который хотите одолжить. Доступны следующие монеты:

- DAI (переменная ставка 5.72%, фиксированная 7.55%)

- USDC (6.5% / 8.22%)

- TUSD (4.98% / -)

- USDT (7.13% / 8.76%)

- sUSD (4.88% / -)

- BUSD (4.31% / -)

- ETH (1.04% / 4.3%)

- LEND (0.01% / 3.02%)

- BAT (0.32% / 3.4%)

- KNC (0.36% / 3.45%)

- LINK (0.2% / 3.25%)

- MANA (3.32% / 7.15%)

- MKR (1.64% / 5.04%)

- REP (0.35% / 3.44%)

- SNX (12.24% / -)

- WBTC (0.44% / 3.55%)

- ZRX (2.47% / 6.09%)

Затем потребуется установить сумму на основе размера депозита, используемого для залогового обеспечения. Выберите стабильную или переменную процентную ставку, подтвердите операцию. Ставку можно потом изменить в любой момент.

Немного о разнице между стабильной и переменной ставкой.

Стабильные ставки не изменяются в краткосрочной перспективе, но в долгосрочной могут быть скорректированы в зависимости от изменений рынка. Что касается переменной ставки, то она основана на спросе и предложении в рамках платформы Aave.

Первый вариант оптимален для планирования суммы выплат по процентам. Второй — для гибкого управления выгодой, поскольку изменения переменной ставки могут существенно повлиять на состояние кредита с течением времени. Переключение между ставками представляет собой эффективный вид финансового планирования.

Фиксированного срока возврата для кредита нет, но задержки по платежам приведут к росту процентов, и рано или поздно это закончится ликвидацией позиции и продажей залога.

На Aave также имеется такое понятие, как health factor (аналог используемого на других площадках LTV) — отношение стоимости залога к кредитным средствам. Чем выше health factor, тем лучше. Если он спустится до 1, то сработает margin call. Тогда можно добавить залога или внести платеж по кредиту, чтобы выровнять ситуацию.

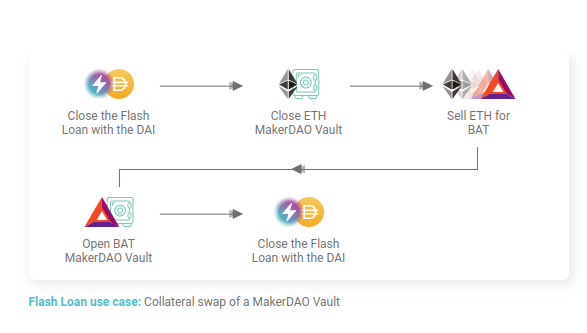

Флеш-кредиты

Флеш кредиты на Aave представляют собой особые необеспеченные кредиты, аналогов которым в реальном мире нет — требуется понимание сути работы блокчейна. Позволяют брать займ на срок до окончания контракта, за это время требуется возвратить и базовый кредит, и проценты

Операции контролируются при помощи LendingPool. Он сравнивает баланс до и после запуска кода, гарантируя, что баланс именно такой, каким был раньше, плюс проценты по флеш-кредиту.

Эта концепция ориентирована на профессиональных разработчиков, которые разбираются в Ethereum, программировании и смарт-контрактах.

Депонирование

Чтобы внести депозит и получать пассивный доход, нужно в личном кабинете зайти в раздел Deposit, выбрать актив, который хотите пустить в оборот, ввести сумму, а затем перевести средства на указанный адрес. С этого момента начнет начисляться процентный доход.

Поддерживаемые монеты и годовые проценты по ним:

- DAI 3.5%

- USDC 3.78%

- TUSD 3.69%

- USDT 5.23%

- SUSD 3.78%

- BUSD 2.86%

- ETH 0.12%

- LEND 0%

- BAT 0.01%

- KNC 0.01%

- LINK 0%

- MANA 1.1%

- MKR 0.49%

- REP 0.01%

- SNX 7.54%

- WBTC 0.02%

- ZRX 0.61%

Вывести депозит можно в любое время на внешний криптовалютный кошелек. Также есть возможность активировать использование депозита в качестве залога в том случае, если понадобится взять кредит.

Комиссии, пополнение и вывод

Чтобы платить по кредиту, достаточно зайти в раздел Borrow и нажать на кнопку погашения у нужного актива. Затем выбрать сумму для возврата и подтвердить транзакцию.

Платформа Aave взимает два вида комиссий:

- С заемщиков взимается 0,25% от суммы кредита. 20% из них отходит партнерам, а 80% обменивается на заимствованную монету и сжигается.

- При взятии флеш-кредитов взимается 0,09% от суммы. 70% распределяется между инвесторами, 30% раздается по описанной в предыдущем пункте схеме 20/80.

Также есть сборы, не зависящие от платформы — это комиссии блокчейна, размер которых зависит от текущей загрузки сети.

Безопасность

Депонированные средства размещаются в DLP (децентрализованном пуле кредитования). Публичный открытый код смарт-контрактов официально проверен и подтвержден независимыми аудиторами. Средства, находящиеся в качестве депозита, можно вывести по первому требованию или перевести на залог по кредиту.

Протокол Aave позволяет любому пользователю взаимодействовать с системой через пользовательский интерфейс, напрямую со смарт-контрактами Ethereum или же по API. Открытый исходный код подразумевает, что на его основе можно создать приложения, полезные для вашего собственного продукта, если возникнет такая необходимость.

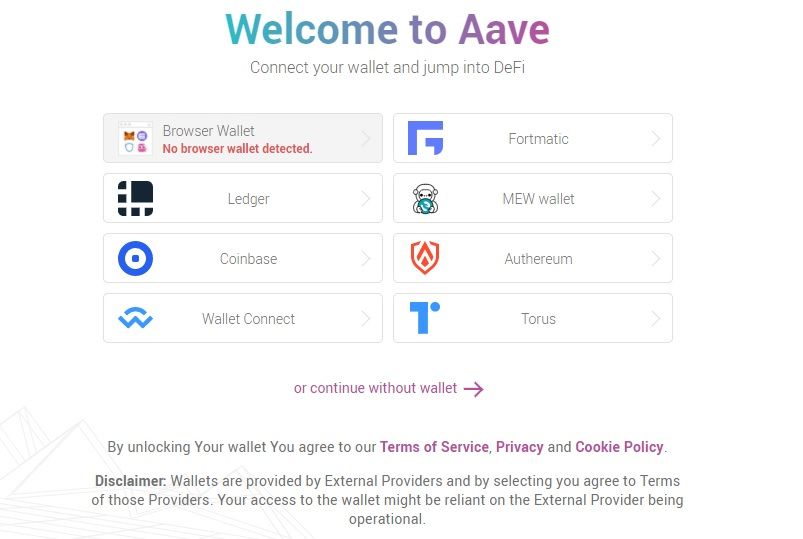

Платформа поддерживает кошельки: Ledger, Coinbase, WalletConnect, Formatic и ряд браузерных кошельков.

Заключение

Главный плюс Aave заключается в максимальной децентрализации. В отличие от конкурентов, эта кредитная платформа не является регулируемым органом, хранящим средства пользователей и передающим отчетность властям, а предоставляет возможность совершать финансовые операции конфиденциально и с минимумом рисков.

How To Use Aave To Lend and Borrow Cryptocurrencies

Crypto lending platforms have acquired a bad reputation, but only in the space of centralized finance. In contrast, decentralized lending protocols like Aave are doing just fine. Learn why that is the case and how to use Aave lending dApp to your advantage.

CeFi vs. DeFi: The Major Differences

Ever since Bitcoin popularized the concept of peer-to-peer money, blockchain developers pushed the envelope further to create an entire ecosystem revolving around cryptocurrencies, otherwise known as decentralized finance (DeFi). The aim is to replicate all the financial services, but in a decentralized manner.

When all is said and done, differences between CeFi and DeFi have come to full light after such an intense string of bankruptcies in 2022:

- Decentralization: Aave is a lending protocol hosted on the Ethereum blockchain. Alongside Bitcoin, Ethereum is the most decentralized network, with over half a million validators. This means there is no central point of control, making the platform resistant to censorship, accessible to everyone, and less susceptible to fraud.

- Accessibility: Unlike regular financial institutions, Aave is accessible to all who have internet access and an Ethereum-compatible wallet. This means there is no checking of one’s credit history or geo-blocking access, which is in stark contrast to traditional banking, which has a wide range of exclusionary criteria.

- Privacy: On a decentralized protocol, your self-custodied wallet is your identity, enabling full ownership. Likewise, Aave doesn’t require users to create an account or share personal information like banks do.

- Transparency: Like all decentralized applications (dApps), Aave runs on smart contracts, making all transactions immutable and transparent, which can then be verified with a blockchain explorer like Etherscan.io. Such a level of transparency doesn’t exist in the banking sector because it relies on government oversight. In DeFi, smart contracts inherently provide an even higher level of scrutiny.

- Cheaper: Because dApps don’t need to maintain costly infrastructure, such as buildings, utilities, tellers, and other employees, Aave can afford to have very low fees. Typically, this is set by the community through governance voting. In the case of Aave, they vote with AAVE coins.

- Flexibility: Quick to adapt to changing conditions with community voting, Aave offers a wide range of borrowing and lending options. This includes flash loans and even credit delegation. The latter enables users to find the lending or borrowing option that best suits their needs.

Now that substantial CeFi vs. DeFi differences are cleared up, it is easy to understand why DeFi is poised to become even more attractive. The Aave DeFi platform is the leading protocol for borrowing and lending. Up until January 2023, Aave holds $5.78 billion in total value locked (TVL). Moreover, Aave spread across six additional chains beyond Ethereum: Avalanche, Fantom, and Harmony, with Polygon, Optimism, and Arbitrum as Ethereum’s scalability networks.

Overview of Aave’s Key Features

The concept of DeFi is simple. Without the reliance on central entities to provide liquidity, users themselves become liquidity providers. Therefore, a dApp is as valuable as the number of people using it. This is otherwise known as the network effect. For instance, anyone can clone Twitter, but that wouldn’t make the clone as valuable because users themselves make it so.

In the case of DeFi protocols like Aave, liquidity without banks is achieved in the following manner:

- Users can deposit dozens of supported cryptocurrencies, from ETH and stablecoins to wrapped Bitcoin (wBTC).

- Those funds are deposited in a liquidity pool, which is just a smart contract tracking funds: how much is deposited by which wallet address.

- The smart contract’s logic also determines the interest rate by which liquidity is extracted from the liquidity pool.

- When borrowers tap into those liquidity pools, they need to supply the collateral.

- The smart contract then locks up that collateral, while issuing yield to liquidity providers (lenders), paid by the borrower.

In essence, every Aave liquidity provider becomes a private virtual bank with Aave protocol as an automated and decentralized facilitator. On the borrowing side of the equation, only certain digital assets can serve as collateral, which is subject to change. Typically, the less volatile an asset is, the more likely it is to be listed as collateral-worthy for obvious risk-mitigating reasons. This is why stablecoins are the most used type of collateral.

The only exception to getting a loan without collateral is the so-called “flash loans.” Aave pioneered flash loans in 2020, allowing users to borrow crypto funds for only a couple of minutes without any collateral.

Such a financial novelty is only possible in the automated world of blockchain and smart contracts. In addition to having a user-friendly interface, Aave also offers a “credit delegation” feature, which allows users to delegate their creditworthiness to others. This feature extends Aave’s flexibility, making it easier for them to borrow funds.

How To Start Using Aave

As with other dApps, anyone can start using Aave with a self-custodial browser wallet like MetaMask or Trust Wallet. This means that there is no third party controlling your funds. However, it is then up to the user to safeguard their recovery phrase and private key.

For example, if it happens that you installed MetaMask on a laptop, and then the house with the laptop is burned to ashes, it is possible to recover the funds. If one remembered the seed/recovery phrase, typically 12–24 words, the wallet address would be regenerated with a new MetaMask installation, enabling access to all the funds.

Step 1: Visit the Aave Platform

With that important note out of the way, it is a simple matter to start using Aave. Go to Aave.com and click on “Launch App” in the upper-right corner.

Step 2: Connect Your Wallet

Once you’ve launched the app, you’ll be taken to Aave’s actual dApp page — app.aave.com. You will then be prompted to “Connect wallet,” also in the upper right corner. Commonly, people select browser wallet → MetaMask as the most popular solution. Otherwise, select the wallet you prefer.

The wallet itself would then prompt a password, if it hasn’t been used in a while. Of course, it would be good if the wallet of your choice is already funded with some stablecoins, or ETH, Ethereum’s native cryptocurrency.

If not, it is a simple matter of transferring funds from one wallet to another, such as Binance to MetaMask, by copy-pasting respective recipient/sender addresses into each one.

How To Use Aave To Become a Lender

Step 1: Check Out the Aave Dashboard

With the entrance into Aave accomplished, you will see Aave’s dashboard divided between “Supply” and “Borrow.” Depending on your needs, and how well your wallet is funded, click on each one to see the list of available assets for both sides of the liquidity equation.

If you’ve been paying attention so far, you already know that “Supply” is for lenders, i.e., liquidity providers, while “Borrow” represents those who wish to take out a loan from the supplied liquidity pools. If you see that either “Supply” or “Borrow” is grayed out for a specific asset, but it has a green checkmark, it means that your wallet is insufficiently funded.

Step 2: Check Out a Liquidity Pool

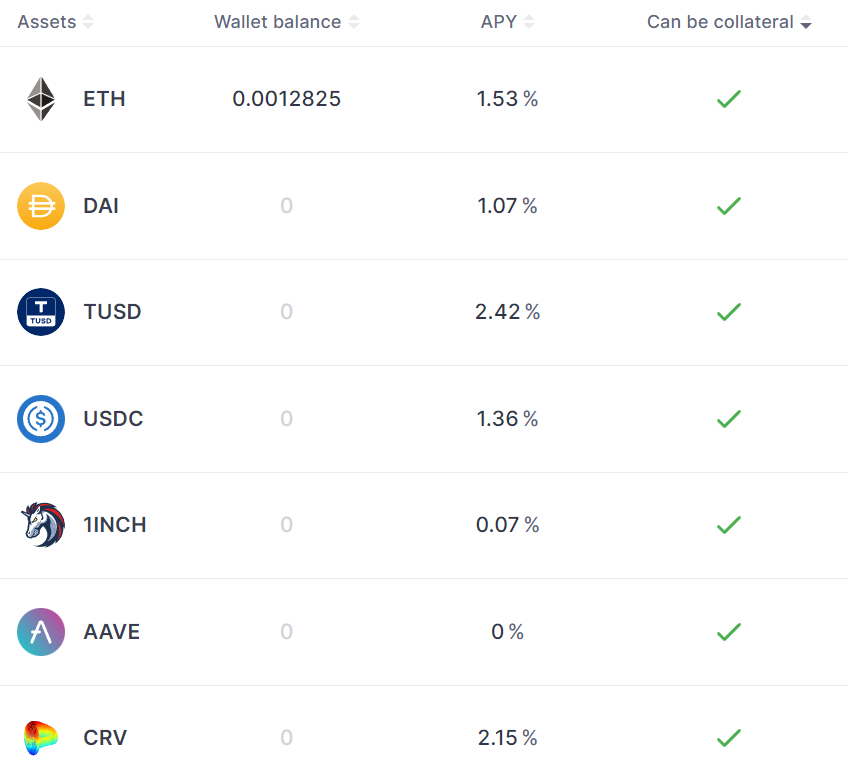

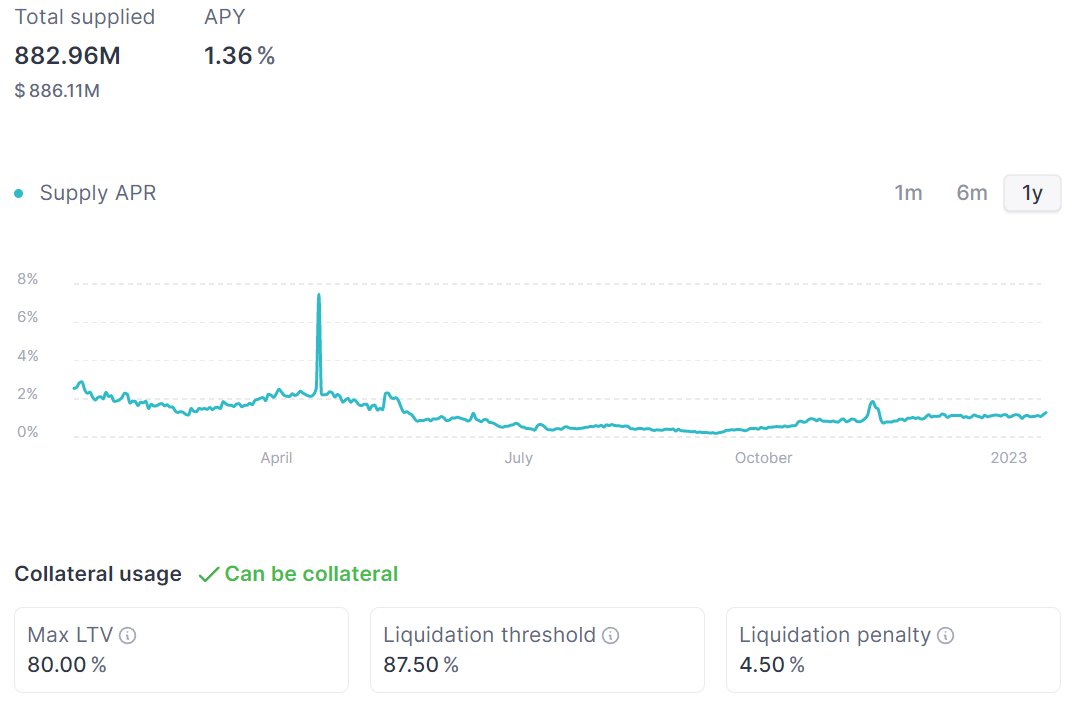

Let’s take a look into one of such liquidity pools by clicking on USD Coin (USDC), a well-regulated stablecoin pegged to the dollar in a 1:1 ratio. Liquidity suppliers have provided 886.11 million worth of USD at an interest rate of 1.36% APY.

Annual percentage yield (APY) measures your return on investment, i.e., on the deposited funds in the USDC liquidity pool. For example, at 1.36% APY, and a deposit of $10,000, you would earn $136 in one year.

However, because APY is a compounding interest, unlike APR, you would be gaining returns on $10,136 if the interest is compounded annually. If it is compounded more frequently, beginning in the first month, the principal would increase to $10,006.12.

For this reason, liquidity providers seek the most frequent compounds. On Aave, compounding frequencies differ based on the asset supplied. It may also change over time.

Aave’s Liquidation Conditions for Borrowers

Because USDC is such a well-regulated stablecoin, lacking volatility, it can be used as collateral, as noted by Aave’s green checkmark. In this section, it is important to understand an asset’s collateral worthiness.

Liquidation-to-value (LTV) measures the risk associated with a loan, otherwise known as collateralized debt position. This measure is expressed as the percentage ratio of the loan amount to the value of the collateral securing the loan.

In the case of USDC, LTV is 80%, which means that if you borrow USDC, you can borrow up to 80% of the deposited USDC collateral. In other words, to borrow $10,000 worth of USDC, at 80% LTV, you would have to deposit $12,000, using the following formula:

Collateral = (Loan Amount) / (1 — (100-LTV Percentage)/100)

Collateral = $10,000 / (1 — (100-80)/100) = $12,000

In addition to LTV, one should also note the liquidation threshold. This is the point at which a loan becomes undercollateralized, therefore, subject to liquidation. Following the previous example, if the value of $12,000 collateral to issue a $10,000 loan, goes under 87.5% ($10,750), the loan could be liquidated at a 4.5% penalty.

Aave’s smart contracts perform this automatically to protect the lender’s funds and the platform itself from defaulting. Typically, only a portion of the collateral will be liquidated to elevate the LTV to a safe level.

For non-stablecoin assets, this becomes dicier because the value of the collateral goes down with the pricing of the asset itself. To track the external pricing of assets, Aave uses Chainlink. This decentralized oracle network feeds off-chain data from exchanges to on-chain smart contracts.

Otherwise, it would be impossible to measure the value of assets and when collaterals should be liquidated.

How To Use Aave To Become a Borrower

Step 1: Examine the Liquidity Pool

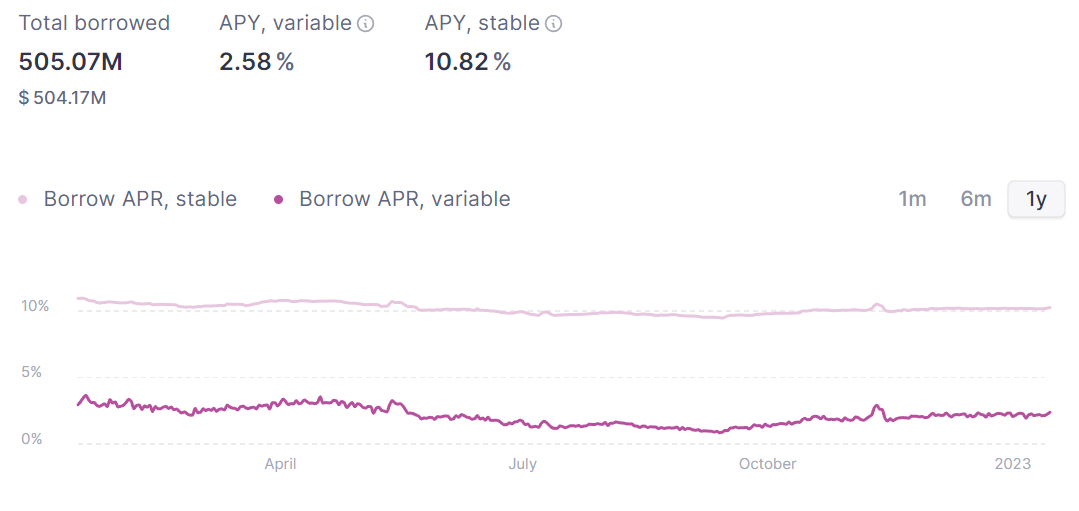

Examining the USDC stablecoin liquidity pool, we can now see what options are available. As you can see, the smart contract for this pool measures how much is borrowed and at which interest rate.

At press time, out of a total of 882.96 million USDC supplied, 505.07 USDC is borrowed. This brings the pool’s utilization rate to 57.21%, telling us what is the capacity for the pool’s loans. At 57.21%, this is the amount of USDC supply available because it depends on liquidity providers.

Typically, if the utilization rate is high, it means that the asset is in demand. In turn, higher demand yields higher interest rates, which is good for lenders but bad for borrowers, who then have to repay their loans at higher rates.

Step 2: Choose Between Fixed and Flexible/Variable Interest Rates

As a result of rate variation in assets, Aave borrowers can pick between two options:

- Fixed interest rate: The interest rate on the loan remains the same for the loan’s entire duration. This way, the borrower knows exactly how much is needed to pay every month, making it easier to budget and plan ahead.

- Flexible or variable interest rate: The interest rate changes over time, depending on the asset’s demand. This rate will fluctuate based on market conditions, such as the price of Ether (ETH), Bitcoin (BTC), or the supplied liquidity in stablecoins.

To avoid surprises, borrowers typically pick a fixed or stable interest rate. In the case of USDC at present time, it is nearly 5x higher than the variable APY. Picking each one depends on one’s perception of the market.

For example, if you expect the borrowed asset, like wBTC, to appreciate in value, it makes more sense to pick a variable interest rate. Additionally, the value of the collateral would also increase.

Conversely, if it is expected that interest rates will rise, such as the Federal Reserve’s funds rate, it would be better to pick a fixed interest rate. Likewise, market conditions could turn unfavorable, regardless of the Fed, so the value of the collateral could decrease. In these scenarios, a fixed interest rate would be constant and easier to plan for.

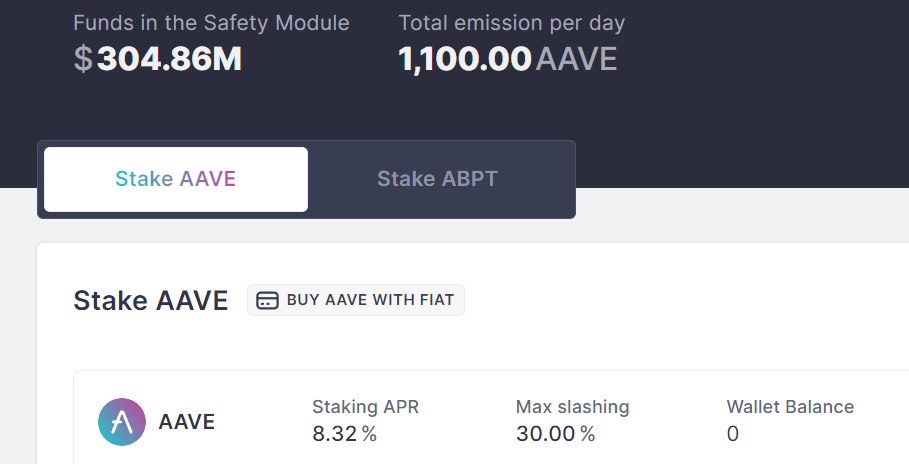

What Is Aave Safety Module?

You may have noticed that the common theme tying all lending threads is risk management. To ensure that the platform remains liquid in adverse market conditions, Aave has integrated the Safety Module, specific to the Ethereum blockchain. Safety Module is a collection of smart contracts that mitigate risk by:

- Ensuring automatic liquidations if the aforementioned LTV ratio goes above a certain threshold.

- Ensuring emergency shutdown in case of a critical bug or code exploit. Then, the platform would temporarily shut down to prevent further damage.

- Ensuring global settlement in the case of a global market crash. In this scenario, Aave’s safety module would settle all outstanding loans and avoid systemic risk.

Aave (AAVE) governance and utility tokens play a key role in the Safety Module. Whenever a loan is liquidated, not only is the portion of the collateral burned, but the corresponding AAVE coins are minted. This process is called a “liquidation incentive.”

The newly minted AAVE tokens are then distributed among Aave token-stakers.

The incentive part comes into play because the more Aave users stake AAVE tokens, the more likely it is they will be selected for loan liquidations, earning them more AAVE coins. This way, Aave liquidity suppliers participate in the risk management of the entire protocol, which is the hallmark of Decentralized Finance (DeFi).

Aave: A Safe and Accessible Choice for Crypto Lending

It is safe to say that 2022 has been the year of the purge of crypto lenders. People have now learned that it makes no sense to replicate centralized governing structure into an ecosystem that began as decentralized. Aave has gone the farthest in mitigating inherent risk associated with loans.

Thanks to its simple, user-friendly interface, crypto beginners can easily navigate and manage their positions. Going the extra mile, Aave’s Safety Module elegantly combines its AAVE governance token to further bolster the platform’s liquidity.

Relying on transparent and automated smart contracts, but enabling financial access to all, Aave puts to shame traditional banking, which relies on fractional reserves and other moral hazards. If you are looking for borrowing without credit checks, Aave is the place to go.

What Is Aave, and How Do You Use It?

Aave is a decentralized lending platform, without a CEO or a bank. It relies on users themselves to provide liquidity for loans. Anyone can access it with a non-custodial browser wallet like MetaMask.

How Do You Make Money on Aave?

You can make money on Aave in three ways. Use flash loans to amplify your arbitrage opportunities. Supply liquidity to earn interest rate. And stake AAVE tokens to bolster the protocol’s security, also in exchange for an interest rate.

How Do I Use My Aave Token?

In addition to using the AAVE token for yield farming, you can use the AAVE token to vote on the protocol’s development proposals, making Aave adapt to changing market conditions. Likewise, whenever loans are liquidated, you can gain AAVE tokens if you have already staked them.

Does Aave Charge a Fee?

Aave has fees that are divided into two categories: flash loans and lending and borrowing. These fees can vary and are determined by governance voting and market conditions.

Can I Trust Aave?

As a decentralized protocol, Aave has already demonstrated resilience as all major centralized crypto lenders collapsed. As long as its underlying network, Ethereum, is not compromised, Aave has a high degree of robustness.

Как взять кредит на DeFi-платформе — личный опыт

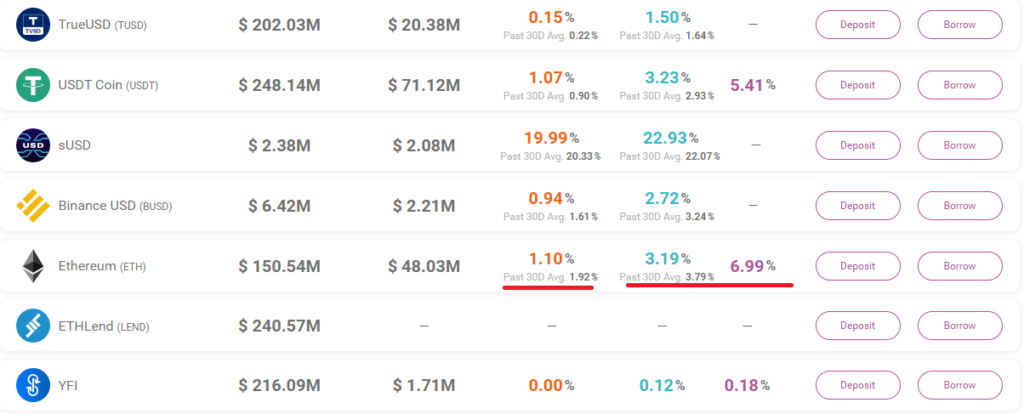

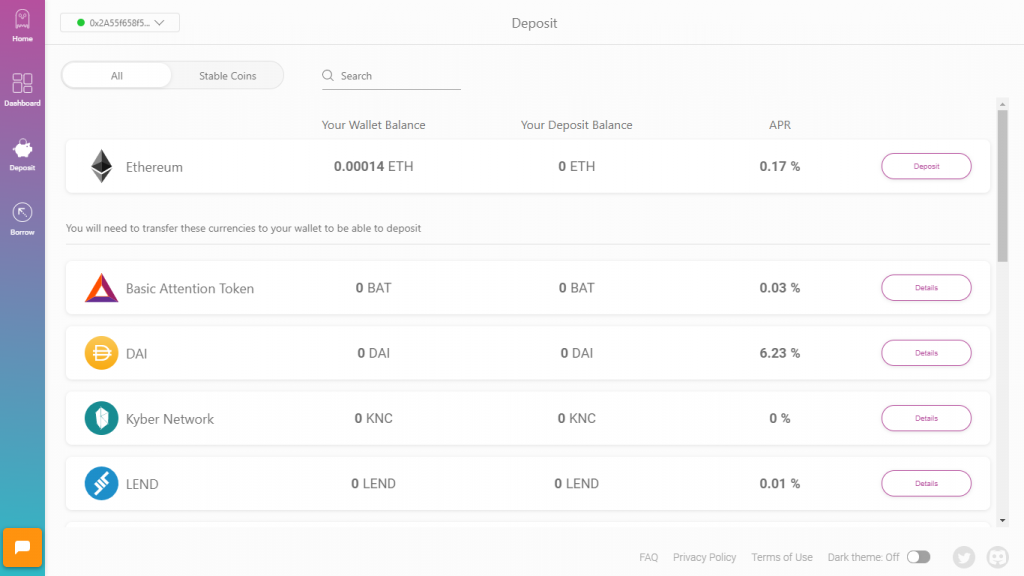

Действительно, платформа Aave готова выдавать кредиты в различных криптовалютах, включая Dai, USDC, TrueUSD, BUSB и других. От выбранной монеты будет зависеть размер депозита и процентная ставка по займу. К примеру, для ЕТН депозит составит 1,10%, а годовая процентная ставка 3,19% (плавающая) или 6,99% (фиксированная).

Шаг 2. Разбираемся в ставках

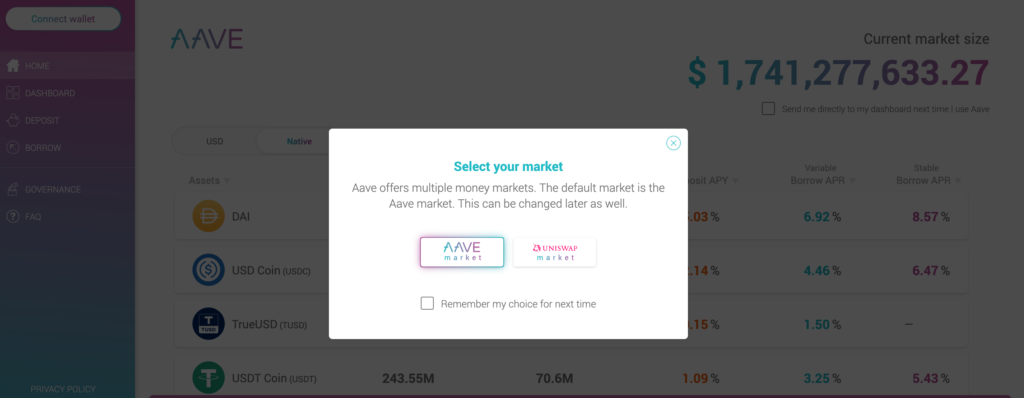

Площадка Aave предлагает два типа ставок: фиксированную и переменную. В чем разница? Фиксированные ставки не меняются на коротком временном интервале, но если рыночные условия резко изменятся, они тоже могут быть скорректированы. Этот вариант удобно использовать, чтобы планировать выплаты. Плавающие ставки меняются в зависимости от спроса и предложения на Aave. Она может варьироваться и становиться более или менее выгодной для заемщика. Пользователи криптовалютный кошелек, можно привязать его напрямую к платформе Aave. Она поддерживает несколько криптокошельков, включая Ledger, Coinbase, Wallet Connect и другие. Но если кошелька нет, можно начать и без него.  Кошелька у меня не было, поэтому я выбрала функцию “Продолжить без кошелька” и перешла на страницу, где нам предлагают выбрать рынок: Aave или Uniswap. С рынками надо разбираться, поэтому я оставила Aave, он был указан по умолчанию. Обещают, что в дальнейшем его можно будет изменить.

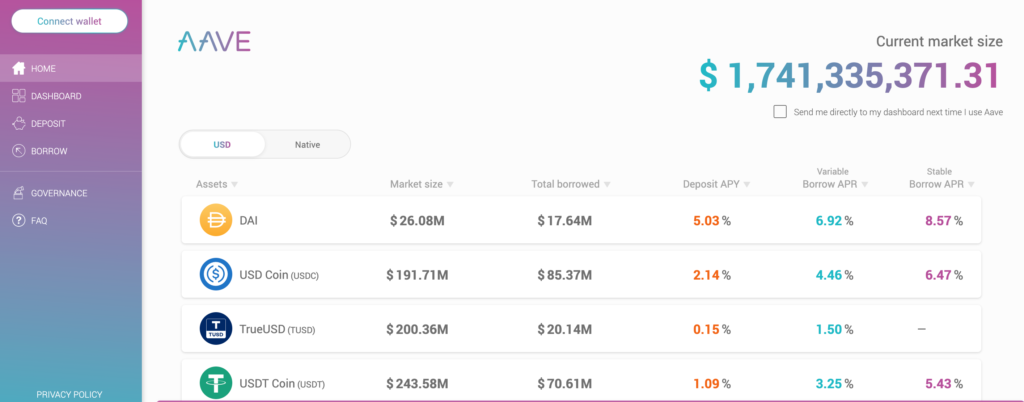

Кошелька у меня не было, поэтому я выбрала функцию “Продолжить без кошелька” и перешла на страницу, где нам предлагают выбрать рынок: Aave или Uniswap. С рынками надо разбираться, поэтому я оставила Aave, он был указан по умолчанию. Обещают, что в дальнейшем его можно будет изменить.  Далее перед нами список токенов, которые можно разместить на депозит или взять в кредит.

Далее перед нами список токенов, которые можно разместить на депозит или взять в кредит.

Шаг 4. Выбираем монету

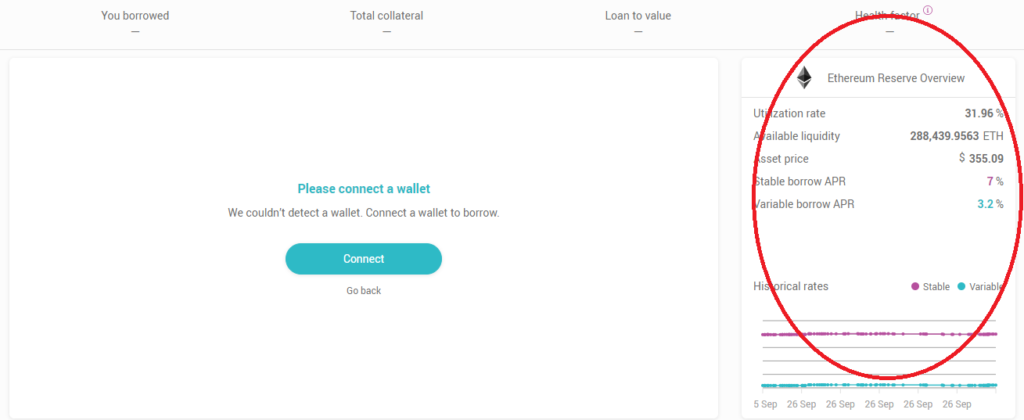

Вот тут-то и выясняется, что кошелек все-таки нужен. Без него в личном кабинете ничего недоступно, зато можно посмотреть условия кредитования под конкретную монету. Мы выбрали ETH и еам предложили кредит в ETH с фиксированной ставкой 7% и плавающей – 3,2%.

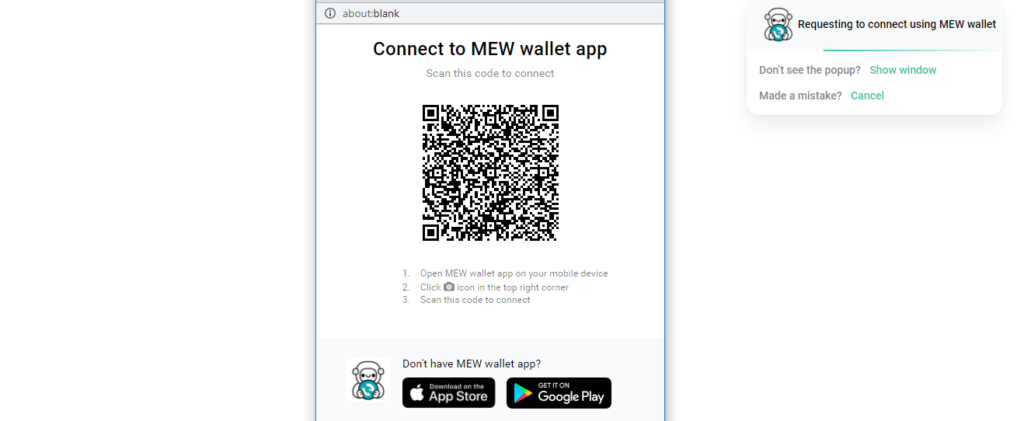

Шаг 5. Подключаем кошелек

Возвращаюсь к подключению кошелька. Для этого нажимаю кнопку “Connect” (см. скрин выше) и меня выкидывает назад, на страницу выбора кошельков. Мне приглянулся MEW, но за милым названием скрывались проблемы. Оказалось, что браузерный кошелек должен обязательно быть связан с мобильным кошельком, иначе у вас ничего не выйдет. Пришлось идти в Apple AppStore и скачивать кошелек MEW.  Дальше – хуже. После считывания QR-кода с помощью камеры телефона, кошелек открывается на самом смартфоне, а не на браузере. Я пробовала несколько раз, но так ничего и не вышло. И это заняло достаточно времени. В конце концов решила продолжить работу в мобильной версии кошелька, так как интегрировать браузерный не получилось.

Дальше – хуже. После считывания QR-кода с помощью камеры телефона, кошелек открывается на самом смартфоне, а не на браузере. Я пробовала несколько раз, но так ничего и не вышло. И это заняло достаточно времени. В конце концов решила продолжить работу в мобильной версии кошелька, так как интегрировать браузерный не получилось.

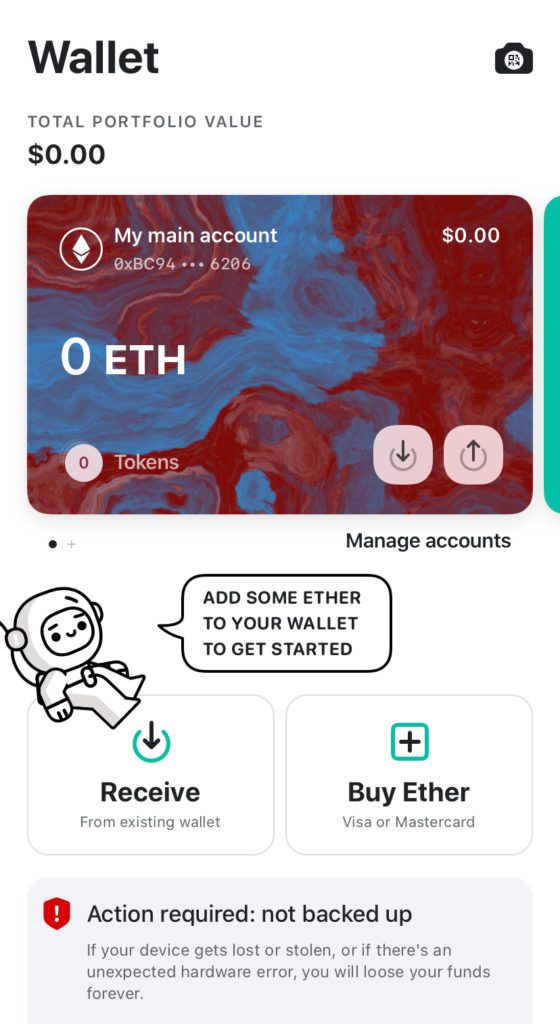

Шаг 6. Пополняем кошелек ЕТН

Наконец-то с кошельком разобралась. Теперь нужно положить на него любую сумму в ЕТН и она должна автоматически отобразиться в личном кабинете платформы, потому что кошелек уже подключен к Aave. Вносим деньги стандартным способом: покупаем с помощью карты или пересылаем из другого кошелька.

Шаг 7. Деньги зачислились в профиль на Aave

После пополнения кошелька деньги автоматически зачислились на счет и отобразились в личном кабинете.

Шаг 8. Берем кредит

Чтобы взять кредит, выбираем функцию Borrow на главной странице или непосредственно в кабинете. />После нажатия на кнопку Borrow открывается страница личного кабинета, где и можно посмотреть условия кредитования: общий доступный объем монет, процентную ставку, стоимость монеты в реальном времени и другое. Указываем сумму, которая нам необходима, и готово! Монеты придут сразу на кошелек, связанный с Aave.

На что обратить внимание:

- Фактор здоровья – это числовое представление надежности ваших депонированных активов по отношению к заемным активам и их базовой стоимости. Чем выше значение, тем безопаснее состояние ваших средств от сценария ликвидации. Если коэффициент здоровья достигнет 1, начнется ликвидация ваших вкладов. DeFi, если можно пойти традиционным путем и оформить кредит в банке”. Но что делать, если банк кредит не дает или дает под огромные проценты, или вовсе отказывает в ссуде из-за плохой кредитной истории. Как раз в таком случае децентрализованные финансы могут стать настоящим спасением. Итак, зачем брать кредит на децентрализованных финансовых площадках:

- можно получить любую сумму на длительный период;

- годовые ставки в разы ниже, чем в банках;

- не нужно собирать справки о доходах, налоговые декларации и другие документы;

- не нужно предоставлять паспорт, ИНН и другие документы, которые содержат личную информацию;

- кредит получает каждый, а сумма кредита напрямую зависит от депозита, внесенного заемщиком;

- деньги приходят насчет моментально. Не нужно ждать неделя рассмотрение заявки и ее одобрения;

- нет залога в виде имущества. Вы рискуете исключительно теми монетами, которые хранятся у вас в кошельке; не имеет границ, поэтому это идеальный вариант для стран с неэффективной банковской системой;

- широкий выбор монет, в которых можно брать кредиты;

- заем и депозит может быть ликвидирован, если цена монеты обвалится;

- рынок криптовалют остается волатильным, поэтому до конца не возможно просчитать годовую ставку, если вы берете кредит с фиксированной ставкой;

- оформление кредита требует некоторых навыков, так как вы сами оформляете и одобряете заявку;

- всегда есть риск взлома протокола и вывода всех средств.

Дисклеймер

Вся информация, содержащаяся на нашем вебсайте, публикуется на принципах добросовестности и объективности, а также исключительно с ознакомительной целью. Читатель самостоятельно несет полную ответственность за любые действия, совершаемые им на основании информации, полученной на нашем вебсайте.